This statement has been attributed to Albert Einstein. Snopes.com can find no evidence Einstein actually said it. However, there is little doubt in my mind that whoever first said it knew what they were talking about."Compound interest is the most powerful force in the universe."

I have written before about the power of compound returns in my blog post, "Confounding Compounding Chronicles". This is one of my favorite compound interest stories from that blog post.

Brutus and Caesar

Caesar was a great politician but like all politicians he had his share of enemies. In order to insure that his children were taken care of if he met an early demise, he instructed Brutus to set up a trust for his children with $1,000 Roman dollars. Of course, Brutus was not the most trustworthy guy. He skimmed off a penny and set up a trust for his own heirs invested in safe government bonds yielding 3%. Caesar's children got $999.99. Brutus left instructions that no one was to touch the money for 2,000 years.

How would that work out? One cent compounded for 2,000 years at 3% would grow to $473,000,000,000,000,000,000,000 ( that is 473 billion billion). The current GDP of the United States is about $15 trillion. In other words, one single penny compounded for 2,000 years would be able to buy everything in the U.S. economy for the next 30 billion years.

If one penny could grow to that sum over the last 2,000 years why isn't there more wealth? The biggest reason is that people rarely can keep their hands off the money. Compounding only works if interest compounds on interest. Most people can't do that. They spend the income as soon as they earn it.

Another big reason is that the original investment capital is lost and the compounding stops with it. Brutus thought he was being smart by investing in the safest investment around-government bonds. Unfortunately, those bonds were Roman Empire bonds. The empire fell apart and the government bonds became worthless. Not only was the compound effect lost but so was the original penny.

***************************************************************

The Brutus and Caesar story really drives home how powerful compound interest is. In fact, it is fair to say that compound interest over time is an impossibility based on the insidious way it works. It is simply so powerful that any borrower who is subject to its terms cannot keep up and will end up being buried beneath it. Anyone paying compound interest eventually cannot run fast enough, or make enough, to pay what is owed.

Those that are successful in fending off the forces of compound interest over the long-term usually do so only because they are able to issue new notes by enticing new lenders to loan them money. They pay off the old notes and interest with promises built on tomorrow and the faith of that lender that the money will be paid off. It often is not.

The end result of this process is default and bankruptcy. This is how the system equalizes. Over time, a lot of borrowed money simply does not get paid back. That is why 1 penny invested 2,000 years ago didn't change the world. The returns on the investment are gone along with the original investment. This is the harsh rule of investing in bonds, stocks or anything else. Money is made and money is lost. There are winners and losers over time.

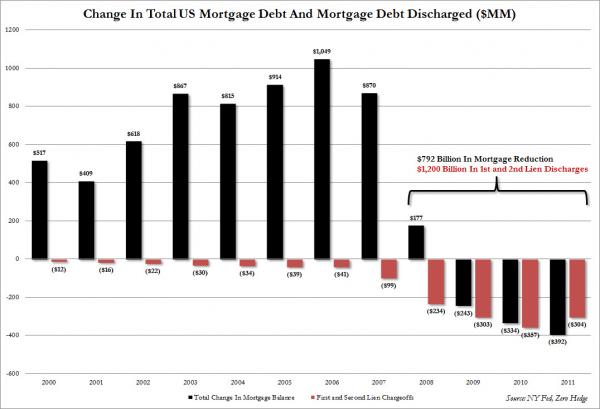

All of this was driven home to me when I saw this post and chart in Zero Hedge on the so-called deleveraging of debt that is supposedly going on among American households. Tyler Durden sets the record straight with the facts which show that it is not deleveraging that is bringing debt levels down but defaults.

Lately there has been an amusing and very spurious, not to mention wrong, argument among both the "serious media" and the various tabloids, that US households have delevered to the tune of $1 trillion, primarily as a result of mortgage debt reductions (not to be confused with total consumer debt which month after month hits new record highs, primarily due to soaring student and GM auto loans). The implication here is that unlike in year past, US households are finally doing the responsible thing and are actively deleveraging of their own free will. This couldn't be further from the truth...

This chart tells the story. Notice that there has been a reduction of almost $800 billion in mortgage debt since 2007 but there has been $1.2 trillion in 1st and 2nd mortgage lien discharges due to defaults. In other words, debt discharges from defaulted mortgages are totally responsible for the reduction in mortgage debt in the United States.

Durden puts it this way.

Instead of actual responsible behavior of paying down debt, the primary if not only reason there has been any "deleveraging" at all at the US household level, is because of excess debt which became insurmountable, not because it was being paid down, the result of which is that more and more Americans are simply handing their keys in to the bank and walking away, and also explains why the US banking system is now practicing Foreclosure Stuffing, as defined first here, as the banks know too well, if all the housing inventory which is currently in the default pipeline were unleashed, it would rip off any floor below the US housing "recovery" which is not a recovery at all, but merely a subsidized bounce, as millions of units are held on the banks' books in hopes that what limited inventory there is gets bid up so high the second housing bubble can be inflated before the first one has even fully burst.All of this brings me back to my original point. Compound interest is deadly when you are on the borrower's side of that equation. And if you are the lender to that borrower you take it in the shorts when default occurs. That $1 trillion in discharges came out of the hide of Fannie, Freddie, your local First National Bank and many more financial institutions who loaned money to home buyers who could not keep up with the original payment terms of the loan.

This is a good lesson to keep in mind when you loan anyone money, whether it is your brother-in-law, a Fortune 500 company or the federal government. History, economics and the power of compound interest tells us that all of the money that is borrowed is not going to be paid back. Proceed cautiously with your money and think very carefully about buying any junk bonds (or Japanese government bonds for that matter) right now. You don't want to be the one holding the bag with nothing in it.

Here is a chart showing junk bond yields. Yields on these high risk loans have dropped to the lowest amount in history. Therefore, those buying these instruments today are receiving smaller compensation for taking this higher risk than ever before. Are we to believe that these loans are that much safer than ever before as the low yields would suggest? Hardly. This is another distortion caused by the Fed's QE policy. Buyer beware!

No comments:

Post a Comment