|

| Credit: https://twitter.com/Barchart/status/1695666793379958985 |

The monthly cost of a house has to come down or rents have to increase. Equilibrium is the natural state.

The biggest problem in housing is that the costs of ownership are outstripping the ability of most households to pay.

The median sales price of a house was 150% of real median household income in 1984.

It is now over 550% of income.

|

| Credit: https://twitter.com/unusual_whales/status/1696174044171862399 |

Values can only be supported if there are people who have the money and income to pay the price of a home or afford the monthly payment.

You get some perspective on how far we have gotten off of a sustainable path with housing costs by considering that we need incomes to spike by 69% or home prices to fall by 41% to bring us back to pre-pandemic affordability.

We could also get there if mortgage rates fell to sub-3% levels again.

What is most troubling is that the affordability index adjustments that are necessary in the United States to get back to pre-Covid levels are even greater than in other major countries right now.

I was surprised to see that the United States is the country that has seen its housing market get the most out of whack since 2019.

However, it is true that the United States had much more affordable housing than almost all other developed countries prior to 2020. Note above that the U.S. was rated 14 on the affordability index pre-Covid while Canada was rated 25, Australia 32 and Korea and New Zealand were 35.

The U.S. is still more affordable than all of these other countries today but the gap has narrowed.

It could be that the U.S. is not going to return to anything that resembles where it was pre-Covid. Housing costs may have been permanently altered at a higher level relative to household incomes.

The one thing that is sustaining housing prices despite the large increase in mortgage interest rates right now is the fact that there are so few houses on the market.

There are fewer houses listed for sale in the United States than at any time in the last 20 years with the exception of April, 2020 when Covid brought the housing market to a halt.

New listings fell 31% compared to a year earlier.

|

| Source: https://www.redfin.com/news/housing-market-tracker-june-2023/ |

Few homeowners are willing to sell and give up a low interest rate mortgage to move up to a house which would carry a higher interest rate and monthly mortgage costs.

Almost 2/3 of homeowners have a mortgage rate below 4%. 91% have a rate below 6%.

Mortgage rates are now higher than they have been at any time in the last 20 years.

Not many homeowners are willing to trade a 4% mortgage rate for a 7%.

The residential real estate market is hovering on the brink of locking up.

Supply is shrinking because existing homeowners don't want to sell because of the low rates they enjoy right now.

Demand is under stress because the high rates are putting more and more houses outside the reach of new entrants into the market.

For now, the limited supply of houses is sustaining the value of homes as demand is still exceeding demand.

What happens if both supply and demand erode even more?

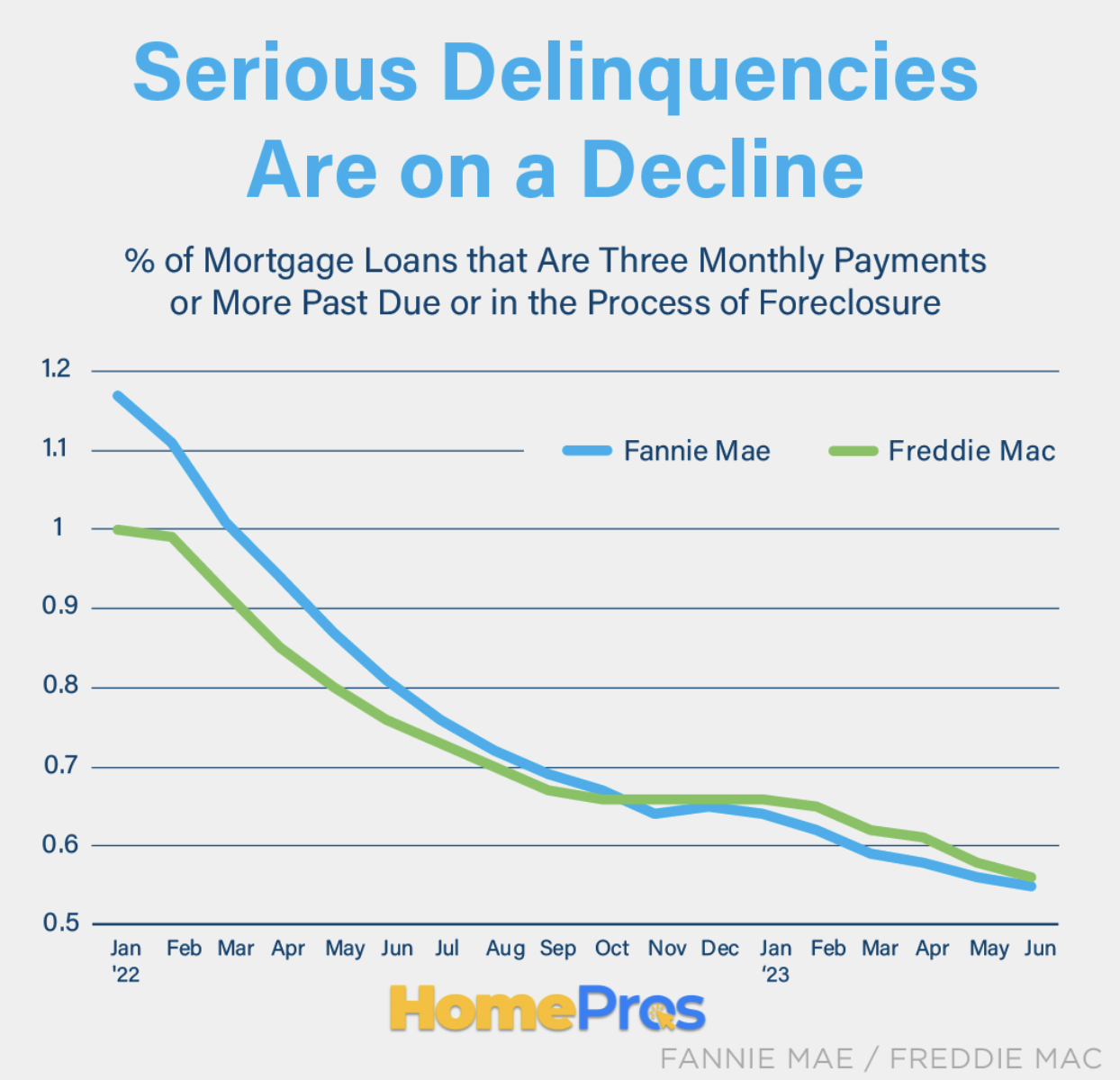

Due to the low unemployment rate and the fact that most homeowners have mortgage rates below 4%, serious delinquencies are very low right now.

What if more people start to be laid off?

Who knows where the housing market goes from here?

Are we going to have to get used to paying substantially more for housing than we have been accustomed to?

Are we going to see rental rates increase substantially in the near future to better match the increase in monthly homeowner costs?

Or will we see monthly home ownership costs start to fall?

This can only occur if mortgage rates and/or home values decline.

All of these scenarios are possible to bring about better equilibrium between home costs and rental rates.

The one thing that most certainly will not occur is a 69% increase in household incomes in the near term.

That you can count on. Everything else is a possibility.

No comments:

Post a Comment