Student loan debt now exceeds $1.1 trillion. Here is a debt clock that shows the approximate amount of student loans outstanding up to the minute. For perspective, total student loan debt was only $763 billion in 2009. Student debt has increased almost 50% in the last four years. All other forms of personal debt, mortgages, auto loans and credit cards, have declined during the Great Recession as I wrote about last year in "Degrees in Debt."

Loan payments are currently being made on just 38 percent of student loans.

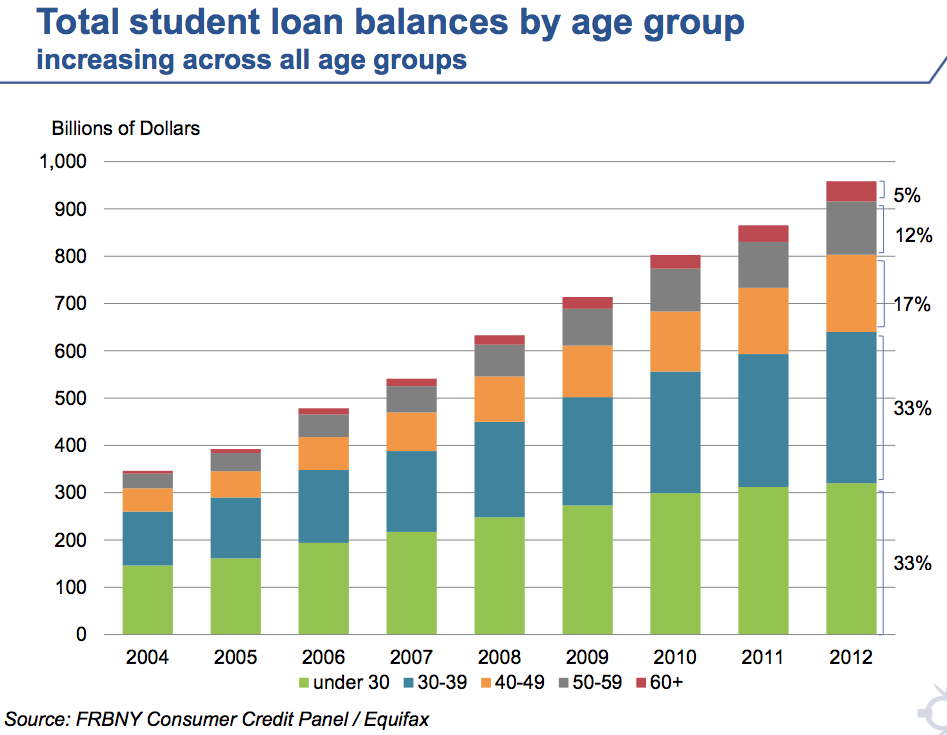

An increasing amount of payments on student loans are being made by individuals in their 50's and 60's. I suspect most of these are parents who co-signed loans for their children.

Bad, Bad Move!

I know that parents love their children and want the very best for them. However, there is no worse situation you can put yourself in heading into your retirement years than to co-sign a college loan.

Before you or someone you know is willing to co-sign on the dotted line, you need to think long and hard about why you are doing it. You also need to make sure the student understands that every dollar borrowed is going to have to be paid back at least two-fold and possibly even more before the slate is marked clean. And federal student loan debt never goes away unless it is paid off. Even in bankruptcy.

Why am I writing about this again?

I happened to hear on the radio last night that over 115,000 Social Security beneficiaries had their monthly retirement benefits garnished to pay student loans last year. That is a staggering number.

Do you know how many had their benefits garnished in 2000? Six! As in 6! As in four less than ten and six more than zero!

How can this happen? The law has been written in its favor. There is no discharge of the debt in bankruptcy and Social Security benefits can be garnished up to 15 percent of the amount you are due in order to offset federal student loan debt.

Would you say that a number of well-meaning parents have gotten burned with co-signing student loans for their well-intentioned children over the last few years?

If I did not have the money to pay for my child's college education and they wanted me to co-sign a loan, I would start by having a real, down-to-earth conversation about the facts of financial life with them. I would steer them to the lowest-cost alternative that was reasonable. If that means two years at a community college for them while living at home, so be it. The first priority is to minimize college costs if you don't have the funds.

I would make sure my child had skin in the game. They would have to commit to a summer job and part-time work to defray a certain percentage of the costs while in school.

If they had poor grades or did not stay on track to graduate in four years, all bets are off as well as my signature on any future loans.

I would say "no way" if they wanted to major in Philosophy, English Literature, Women's Studies or something similar where it is hard to see a wealth of job opportunities after graduation. If your student does not have a good paying job after graduating with one of these degrees you are almost certainly going to have to cover that loan as a co-signer.

Paul Oster, a credit expert, suggested a few other student loan tactics in a column in The New York Daily News that might be helpful to avoid putting your Social Security at risk when co-signing a loan.

Parents should know that a student loan is not dischargeable under bankruptcy law. You can have your mortgage, car loan, and credit cards all forgiven if you filed bankruptcy, but you would still be responsible to pay back your student loans.

You should assume that if you co-sign, you will be paying the entire monthly payment. Here are some of my recommendations:

*Don't borrow more than you need.

*Have an emergency fund to cover six months' worth of payments.

*If your child earns income as a student, make sure a small portion of that pay goes into that emergency fund.

Perhaps the most important tip I would give parents relates to who should be making the payments. While your child is the official borrower, I would encourage you to be the one sending checks to the lender. In turn, your child should be paying you.

Why? Parents need to monitor and control loan payments to protect their own credit profile.

Unfortunately, we have seen the devastating effects that missed student loan payments can have on parents' credit scores. Most of the time parents are not even aware that there has been a missed payment until they apply for a loan themselves.

At that point, it's far too late and the damage to the credit score has been done. A one-time, 30-day delinquency can drop credit scores by as much as 100 points.

Student loans have become a necessary evil in today's world. A student loan can have a dramatic effect on the credit and monthly budget of parents and their children.

Often it is a young person's first encounter with a credit obligation. It needs to be carefully considered.

Of course, the easiest way to avoid the problem of student loans is to plan ahead. Save early and save often. Get compound returns working for you.

I generally put all my children through college with an investment of less than $10,000 for each of them. Of course, most of that went in when they were younger than 5 years of age. I also had the benefit of a strong bull market during most of the 1980's and 1990's that allowed those funds to compound at double-digit returns in equity mutual funds for close to two decades. Money multiplies quickly when you have that formula working for you.

The future may not be as kind. However, borrowing money is never kind. Avoid it at all costs, especially if you are a co-signer. Social Security's returns are bad enough now for the Baby Boom Generation and those born later. Don't make it worse by having to pay off a student loan with it as well.

No comments:

Post a Comment