Conventional wisdom has long held that you should buy a home as soon as you can.

"It is better to own that rent."

"If you rent you are just throwing your money away."

Of course, this financial advice ignores several underlying truths.

If you buy a house and take out a 30 year mortgage a large portion of the money you pay each month is going to pay interest in the beginning. You are building little equity in the first years you are in the house.

In effect, the interest payments are not much different than rent payments.

For example, this is the amortization schedule on a $200,000 loan at a 6.86 interest rate for the first five years of a 30-year mortgage loan.

Despite $63,000 being paid on the mortgage less than 15% of the total payments goes to pay down the balance by year 5 (less than $10,000 on the $200,000 loan).

|

| Source: https://www.calculator.net/mortgage-amortization-calculator.html |

Second, owning the house also makes you responsible for real estate taxes, insurance and repair costs that you don't have as a renter. These costs quickly add up.

Finally, if you buy a house and find that you will have to move within the first three years, the odds are high that you will not make any money on the house.

Housing prices have historically averaged about a 4% annual increase over the last 100 years. The last 50 years have been better (a little over 5%) thanks to low interest rates but real estate returns have still lagged stock and bond returns by significant margins over the last 50 years.

|

| Source: NYU Stern School |

When you take account of transaction costs in getting into and out of a house, you need close to a 10% increase in value just to cover transaction costs if you are in a house only a few years.

Of course, the increase in the value of houses over the last three years has been much higher than 4%-5% per year.

Does that suggest that we can expect housing values in the next few years to moderate or even fall?

That has to be a concern to anyone looking at the housing market right now.

For example, it is a rule of thumb that you should not spend more than 28% of your income on a mortgage payment. Spending more than this does not leave much flexibility to pay for the other necessities of life (food, utilities, transportation) not to mention taxes, insurance and saving for retirement.

There are now 30 states in the United States where the average mortgage payment on a median priced home is at least 30%.

Considering this data it should probably not come as a surprise that the Federal Housing Administration (FHA) has just approved 40-year mortgages beginning in May.

|

| Source: https://www.abc15.com/news/state/fha-approved-40-year-mortgage-for-homebuyers-in-may |

On the mortgage example above, a 40-year mortgage would decrease the monthly mortgage payment by $89/month but would result in an additional $115,000 in interest over the life of the loan.

How is this "innovation"going to really help anyone?

Housing affordability is even worse in Canada.

General inflation and real incomes are both up +149% since 1976 in Toronto.

Housing prices are +1,840%!

The monthly mortgage payment on the median priced single family home in Toronto is now more than the median income in Toronto!

|

| Source: https://twitter.com/daniel_foch/status/1608449814186045440/photo/1 |

Notice in that graphic that it is projected that it would take 30 years for those with an average income to accumulate the funds necessary for a down payment if they save 10% of their income for that purpose.

A representative home in Toronto now costs more than $1.3 million.

Look at the bottom graphic to see how mortgage payments have increased from about 50% of income to 100% of income in Toronto in the last two years.

|

| Source: https://twitter.com/daniel_foch/status/1608449814186045440/photo/1 |

Indeed, how is that mathematically possible or sustainable?

You have to believe that something has to give in Canada (and in the United States).

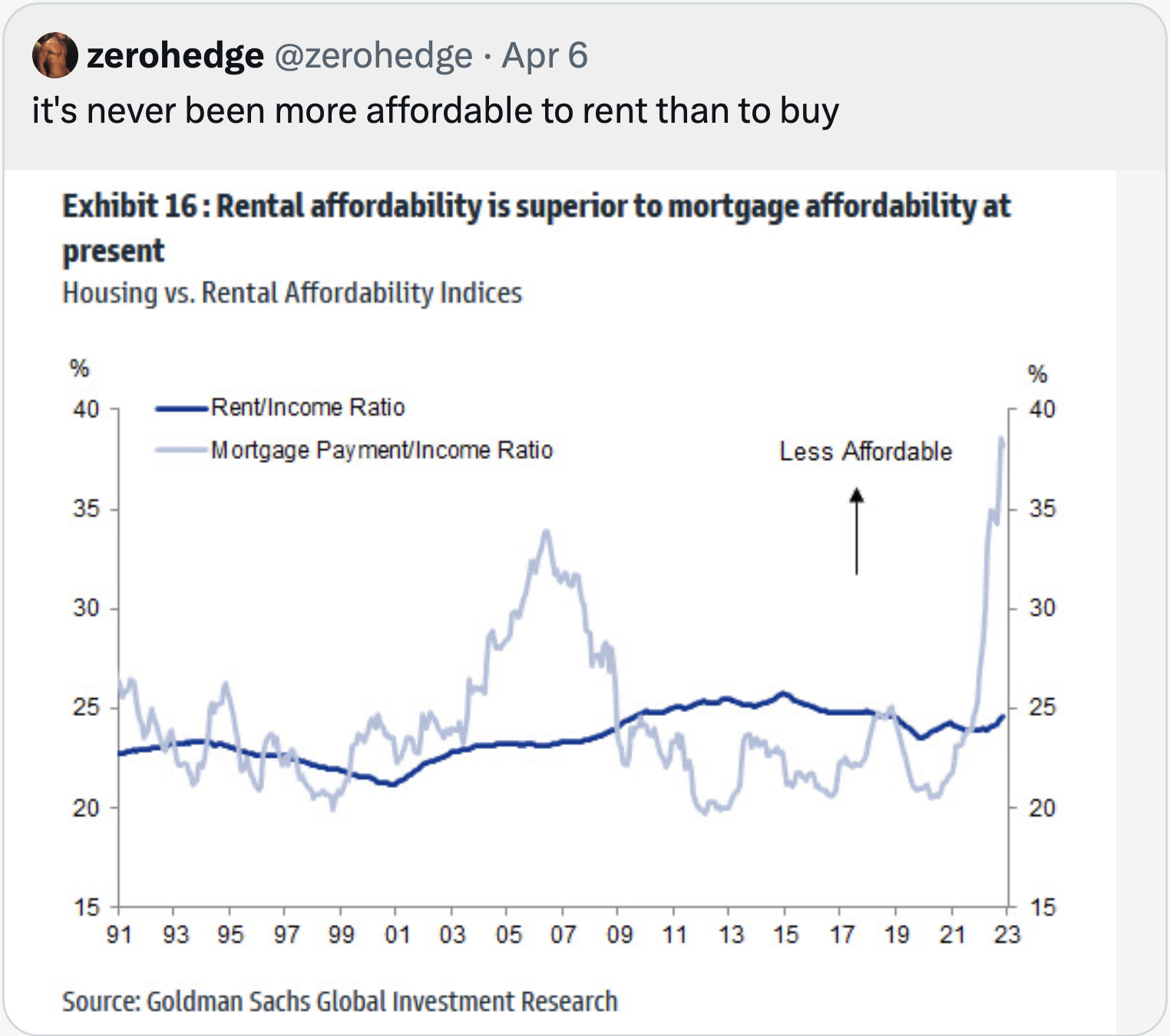

We are likely to see more people renting because right now it has never been more financially advantageous to rent in the United States.

In the United States we are also seeing a surge in the construction of multi-family units unlike anything we have seen in the last 50 years.

|

| Credit: https://twitter.com/nickgerli1/status/1641203294755516416 |

When you see the current disconnect between mortgage payments and rents the natural order suggests that mortgage payments have to come down (as they did after 2007) or rents have to increase to be in some type of equilibrium.

However, there is currently a low supply of houses for sale in most parts of the country that is keeping home prices from falling and the increasing supply of new apartments may restrain rents from increasing.

|

| Housing Inventory for Sale 1982-2023 |

This may mean that the disconnect between mortgage payments and rents could endure longer than we might normally expect.

Nevertheless, when anything is out of balance there are many forces at play to bring things back in balance.

You can expect the same in the relationship between mortgage payments and rents.

The end result may be deferred but you can only deny the reality of the numbers so long.

The mathematics and the economics of supply and demand will always win in the end.

No comments:

Post a Comment